International Trade in the Contemporary history – Trade History

How did Modern International Trade begin?

Introduction

The Contemporary Era, spanning from the late 18th century to the present, has witnessed a radical transformation in international trade. This period is characterized by industrialization, globalization, the rise of new economic powers, and the establishment of international organizations that regulate global commerce. In this post, we will explore how international trade has evolved during this era by analyzing the key events, actors, and their economic and social impacts. (For a broader context, feel free to review our previous articles on the origins of trade—from its primitive beginnings, through ancient and medieval commerce, to the Modern Age’s international expansion.)

International trade in the Modern Age

The origin of International Trade

Trade of ancient civilizations

The Middle Ages and international trade

1. The Industrial Revolution and International Trade

Impact of Industrialization

The Industrial Revolution, which began in Great Britain in the late 18th century, marked a turning point in international trade. The introduction of new technologies and production methods increased manufacturing capacity and reduced costs, enabling large-scale commerce. This transformation not only affected national economies but also fundamentally altered the structure of global trade.

Technological Innovations

Telegraph: The telegraph enabled near-instantaneous communication across continents, improving coordination in international commercial activities.

Railroads: The development of railroads allowed for the rapid and efficient transport of goods over long distances within countries.

Steamships: The advent of the steamship revolutionized maritime transport, drastically reducing shipping times and costs.

These innovations expanded markets and facilitated the integration of economies on a global scale.

Expansion of Markets

Industrialization led to the creation of new markets and increased demand for raw materials. Industrial powers such as Great Britain, France, and Germany sought colonies and territories that could supply the necessary resources to sustain their growing industries. This search for raw materials and new markets spurred international trade and fostered greater economic interdependence among nations.

Historical Examples:

- Great Britain and Cotton: Britain imported vast quantities of raw cotton from the United States and India, which was then processed in its factories into textiles that were exported worldwide.

- Germany and Coal: Rich in coal and iron, Germany used these resources to develop its heavy industry, expanding the trade of steel and industrial machinery and establishing itself as a leading industrial and commercial power.

Changes in Economic Structure

The Industrial Revolution transformed national economies from predominantly agrarian systems to industrial ones. This shift drove international trade as industrial economies needed to export manufactured goods and import raw materials. Specialization in the production of certain goods also led to greater efficiency and competitiveness in global trade.

Social Effects

The surge in international trade during the Industrial Revolution had significant social implications. Urbanization increased as people migrated to cities in search of factory work, leading to the growth of a new urban working class. While international trade and industrialization brought prosperity to many nations, they also resulted in harsh working conditions and rising economic inequality.

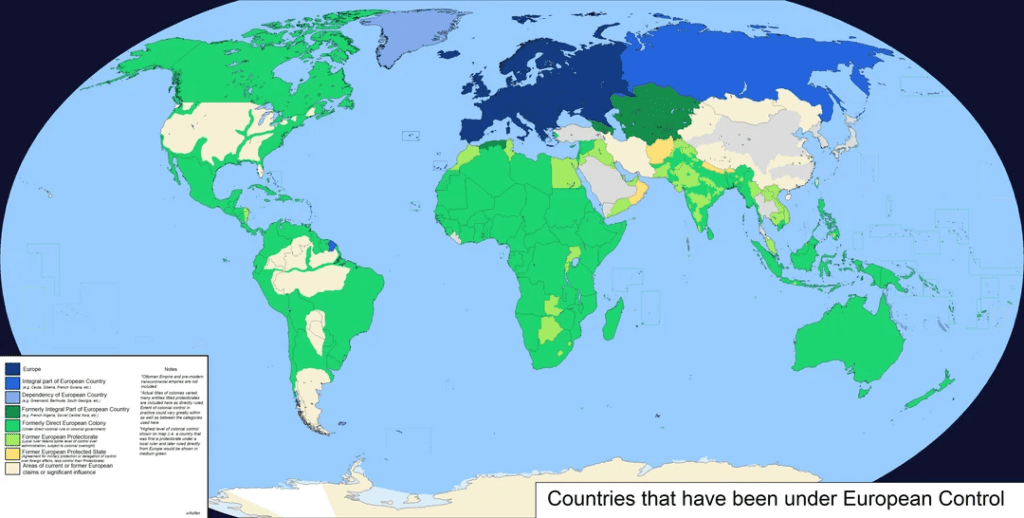

2. The Age of Imperialism and Colonialism

European Imperialism

In the late 19th and early 20th centuries, European powers, along with Japan and the United States, embarked on an era of imperial expansion. This period saw the annexation of vast territories in Africa, Asia, and Latin America.

Economic Impact

Imperialism facilitated direct access to natural resources and new markets, which was crucial for sustaining industrial economies. However, it also led to the exploitation and subjugation of local populations, profoundly altering their economies and social structures.

Conflict and Competition

The scramble for territories and resources often resulted in conflicts among imperial powers, such as the Boer War and the Opium Wars. These tensions contributed to global instability and laid the groundwork for larger conflicts in the 20th century.

3. The 20th Century: World Wars and Reconstruction

World Wars

The two World Wars had a devastating impact on international trade. The destruction of infrastructure and economies led to a significant decline in global commerce.

- World War I: Trade plummeted due to naval blockades, export restrictions, and the destruction of commercial fleets.

- World War II: These issues worsened during the Second World War, leading to an almost complete halt of global trade in several regions.

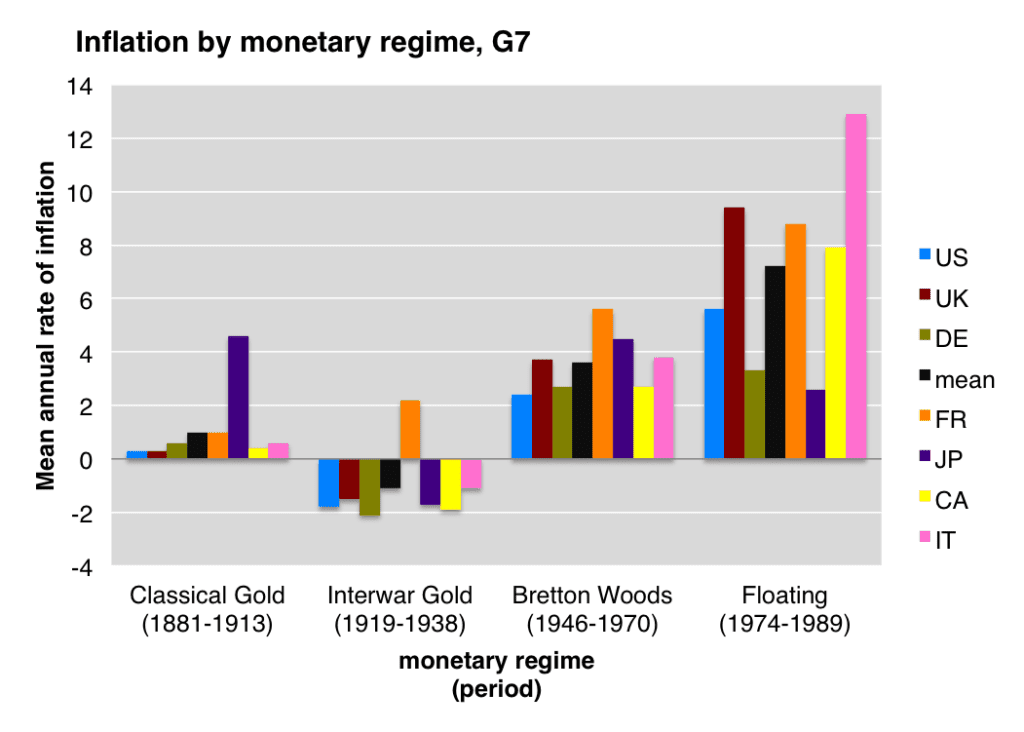

Reconstruction and Bretton Woods

After World War II, the 1944 Bretton Woods Conference established a new international economic order. Institutions such as the International Monetary Fund (IMF) and the World Bank were created to promote economic stability and international cooperation. The Bretton Woods system also introduced the U.S. dollar as the international reserve currency, linked to gold, which stabilized exchange rates and facilitated global trade.

The Marshall Plan

Launched in 1948, the Marshall Plan was a massive U.S.-led economic assistance program aimed at rebuilding Western Europe. This initiative not only revitalized war-torn economies but also jump-started international trade by reestablishing trade networks and positioning European economies as key global trading partners.

Free Trade Agreements

The General Agreement on Tariffs and Trade (GATT) of 1947, which later evolved into the World Trade Organization (WTO) in 1995, set out rules and norms to facilitate international trade by reducing tariff barriers. GATT negotiations led to significant tariff reductions and the elimination of non-tariff barriers, fostering an environment of free trade.

The post-war reconstruction, combined with free trade agreements, resulted in a marked increase in international trade. Western European economies, Japan, and other nations recovered and grew, creating a tightly interconnected global trade network that laid the foundation for late-20th-century globalization.

4. Globalization and New Economic Powers

Globalization

In the late 20th and early 21st centuries, globalization accelerated international trade. The reduction of trade barriers, advances in technology, and the liberalization of financial markets enabled unprecedented economic integration. Globalization is characterized by the interdependence of national economies and the growing importance of multinational corporations.

New Economic Powers

Countries such as China, India, and Brazil emerged as economic powerhouses, transforming the global trade landscape. China, in particular, became a central player after its accession to the WTO in 2001—a landmark moment in globalization. Rapid industrialization and economic growth turned China into the “world’s factory,” exporting vast quantities of manufactured goods.

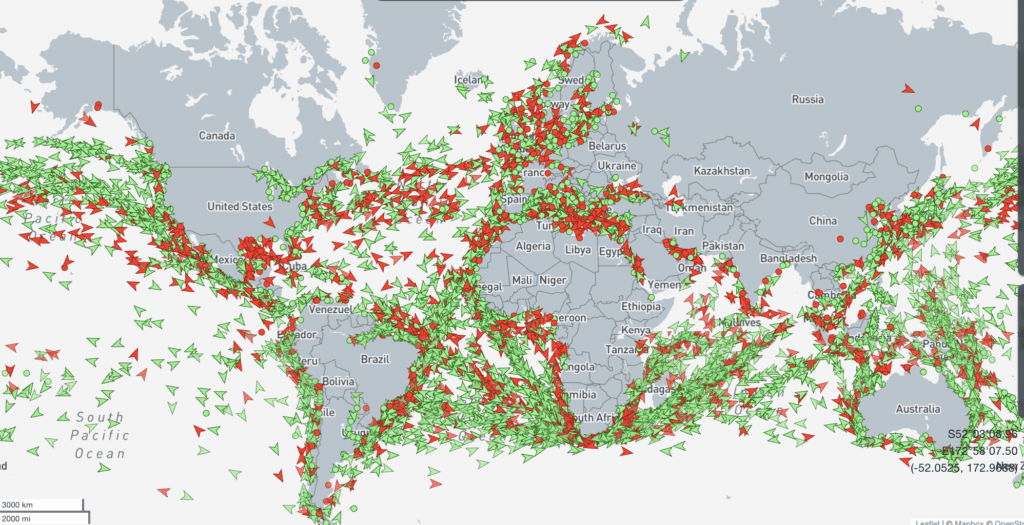

Global Supply Chains

Globalization also led to the development of complex global supply chains, where the production of goods is distributed across multiple countries to optimize costs and efficiency. Multinational companies established factories and production centers around the world to take advantage of each region’s comparative advantages. For example, electronic components might be manufactured in Asia, assembled in Latin America, and sold in European and American markets.

Economic Impact

Globalization has had a profound impact on the world economy. It has spurred rapid economic growth in many developing countries, lifting millions out of poverty. However, it has also generated challenges such as economic inequality and vulnerability to global financial crises. Intense global competition has led to job outsourcing and downward pressure on wages in certain sectors.

Regulation and Fair Trade

The rapid growth of global trade has also brought increased attention to regulation and fair trade practices. International organizations like the WTO work to establish standards and resolve trade disputes, while a growing fair trade movement seeks to ensure that producers in developing countries receive equitable prices and that labor and environmental rights are respected.

5. Challenges and Opportunities in the 21st Century

Protectionism and Economic Nationalism

Despite the benefits of globalization, the 21st century has seen a resurgence of protectionism and economic nationalism. Trade disputes—such as the trade war between the United States and China—have created uncertainty in global commerce. Protectionist policies, including tariffs and trade restrictions, aim to shield domestic industries but can provoke retaliatory measures and reduce global trade.

Global Financial Crisis

The global financial crisis of 2008 served as a stark reminder of the interconnectivity and vulnerability of the world economy. Originating in the United States’ financial sector, the crisis quickly spread to other countries, impacting economies worldwide. Although recovery was slow and uneven, the crisis prompted a reevaluation of economic policies and increased international cooperation to prevent future financial meltdowns.

Technological Innovations

Technology continues to transform international trade. Digitalization, e-commerce, and emerging technologies such as artificial intelligence and blockchain are reshaping business practices. E-commerce platforms have enabled small and medium-sized enterprises to access global markets, while blockchain promises enhanced transparency and efficiency in global supply chains.

Sustainability and Trade

Sustainability has become a central concern in international trade. Companies and governments are increasingly committed to sustainable business practices that minimize environmental impact and promote social responsibility. Modern trade agreements often include provisions on environmental protection and labor rights, reflecting the growing emphasis on sustainability.

Regional Trade Agreements

Regional trade agreements, such as the North American Free Trade Agreement (NAFTA) and the Regional Comprehensive Economic Partnership (RCEP), are playing an increasingly important role in global commerce. These agreements aim to facilitate trade among member countries by reducing tariffs and non-tariff barriers, promoting economic cooperation, and strengthening regional commercial ties.

References:

Obstfeld, M., & Taylor, A. M. (2004). Global Capital Markets: Integration, Crisis, and Growth. Cambridge University Press.

Landes, D. S. (1969). The Unbound Prometheus: Technological Change and Industrial Development in Western Europe from 1750 to the Present. Cambridge University Press.

Hobsbawm, E. J. (1987). The Age of Empire: 1875-1914. Weidenfeld & Nicolson.

Eichengreen, B. (1996). Globalizing Capital: A History of the International Monetary System. Princeton University Press.

Baldwin, R. (2016). The Great Convergence: Information Technology and the New Globalization. Harvard University Press.

Rodrik, D. (2011). The Globalization Paradox: Democracy and the Future of the World Economy. W. W. Norton & Company.

Williamson, J. G. (1996). Globalization and Inequality Then and Now: The Late 19th and Late 20th Centuries Compared. NBER Working Paper.

Frieden, J. A. (2006). Global Capitalism: Its Fall and Rise in the Twentieth Century. W. W. Norton & Company.

Findlay, R., & O’Rourke, K. H. (2007). Power and Plenty: Trade, War, and the World Economy in the Second Millennium. Princeton University Press.